In light of last week’s CPI print and the ongoing third quarter earnings season we want to share a market update with historical perspective. We also want to highlight our portfolio positioning and outline the key factors that could drive a sustainable and positive turnaround for equities.

In summary, we are defensively positioned, poised to benefit from recovery upside and are watching new opportunities closely as they emerge. We need to see a more convincing slowdown in inflation before the federal reserve can ease their rhetoric (which will be a positive driver for stocks).

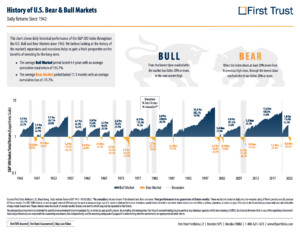

Market update and historical perspective

- The S&P500 is now trading only 6% above pre-pandemic levels and is down ~25% for the year. Reasons for this include a sharp rise in interest rates, high inflation, Russia’s war on Ukraine, expectations of an economic slowdown and more.

- Interest rates are likely to continue rising at least until the end of this year and the economy is likely to slow down further (though consumers are still spending savings accumulated over the pandemic, which is driving solid consumption). Inflation remains well above the feds 2% target and is gradually slowing down. By extension, interest rates are unlikely to continue rising next year with the velocity we have seen so far in 2022.

- There’s been an increase in negative sentiment in the media recently as the S&P500 has moved lower. News is typically a lagging indicator that reports about events that have already happened and sometimes makes predictions about what might happen.

- The stock market on the other hand is already ~25% down this year and is a leading indicator that looks into the future to assess the impact of events that have occurred and are expected to occur.

- The median bear market return since 1929 is -34% (we are already down ~25% in 2022). The median historical return as we cycle out of a bear market and into a new bull market is a lot higher at 122%.

- Since 1926 bear markets have on average lasted 1.3 years, while bull markets have on average lasted a lot longer at 6.6 years. Since the end of WWII, the median peak to recovery period for S&P500 bear markets is two years (we are almost one year off the S&P500 peak in December 2021).

Source: First Trust Portfolios

Portfolio positioning

- We have been expecting inflation to remain relatively high and for interest rates to continue rising and have been defensively positioned with overweights to quality high dividend companies and structured yield notes.

- We continue to manage risk in the near term through structured hedged notes with confidence in our long-term investments in high quality companies.

- We have made changes over the course of this year to ensure we have low exposure to long duration assets in our fixed income portfolio and are mostly invested in shorter duration bonds that are less price sensitive to increases in interest rates.

- We are reducing our exposure to cyclical companies as we are seeing signs that the interest rate increases are likely to change consumer behavior (likely over the course of the next year). We are adding proceeds to our positions in good quality defensive companies trading at attractive prices and are poised to benefit from any recovery upside.

- Some long duration treasury bonds are down in the 30% range so far this year as yields have moved higher. When the fed stops increasing interest rates, we think there will likely be an attractive opportunity to increase exposure to long duration bonds with higher yields and solid recovery upside. We are watching this closely.

- We are data driven and will look to pivot our equity allocation more aggressively to capture recovery upside when appropriate.

What could drive a sustainable rally for equities?

- The first thing we want to see are convincing signs that inflation is set to move meaningfully lower. We are watching closely for signals in the consumer, the supply chain, the labor market, housing, energy, the rental market, in goods and services and more.

- When inflation starts to move meaningfully lower, the fed will be able to slow down the pace of their interest rate rises and eventually start to cut interest rates again (which is positive for equities).

- The next fed meeting is on November 2 and the likely outcome is a 0.75% interest rate increase. We will be watching their commentary – if the fed hints at not only watching inflation but also the impact of interest rate rises on the economy, that would likely be received positively by the equity market.

If anything specific to your situation has changed, please feel free to reach out and we can have a conversation. Next week we will be releasing our quarterly market outlook where we will share deeper insights on the state of the economy and markets.

This material provided by Gentry Private Wealth, LLC (“GPW”) is for informational purposes only. It is not intended to serve as a substitute for personalized investment advice or as a recommendation or solicitation of any particular security, strategy or investment product. Opinions expressed are based on economic or market conditions at the time this material was written. Economies and markets fluctuate. Actual economic or market events may turn out differently than anticipated. The material has been gathered from sources believed to be reliable, however GPW cannot guarantee the accuracy or completeness of such information, and certain information presented here may have been condensed or summarized from its original source. GPW does not provide tax or legal or accounting advice, and nothing contained in these materials should be taken as such. As always please remember investing involves risk and possible loss of principal capital and past performance does not guarantee future returns; please seek advice from a licensed professional. GPW is a Registered Investment Adviser. SEC Registration does not constitute an endorsement of GPW by the SEC nor does it indicate that GPW has attained a particular level of skill or ability. Advisory services are only offered to clients or prospective clients where GPW and its representatives are properly licensed or exempt from licensure. No advice may be rendered by GPW unless a client service agreement is in place. GPW and GoalVest Advisory are independently owned and operated.