The Advisor, November 2022

November 1, 2022

To many of us, November is a month to be thankful. We encourage you to take a moment to reflect and ask yourself: What are you thankful for this year?

Gentry is grateful to you for your continued support even in these difficult economic times. We are also grateful for our dedicated partners, associates, and staff that make running our firm possible. Each person has a unique and critical role in our team that helps us keep providing comprehensive wealth management services to our clients. We encourage you to take a few minutes to reflect and focus on the positive.

As earnings season is off to a good start, the S&P 500 is up 3.9% over the last week (as of 10/27/2022). Inflation remains well above the Federal Reserves’ 2% target and poses the most important challenge in markets today. While inflation has moved lower over the quarter, we still need to see more substantial moderation before the Fed can ease up on the policy. Consumer spending remains solid as households continue to spend excess savings accumulated during the Pandemic. While third quarter GDP is likely to be positive, leading indicators are pointing towards a slowdown in economic activity next year. We expect quantitative tightening to continue and interest rates to move higher through the end of the year, as the Fed appears set to raise interest rates at their November 2nd meeting.

We continue to maintain our defensive positioning in our equity allocation by being overweight value equities and implementing portfolio hedges with quality dividend companies. In our fixed income allocation, we are underweight long duration bonds and low-quality credit and are increasing the size of underweight to long duration bonds.

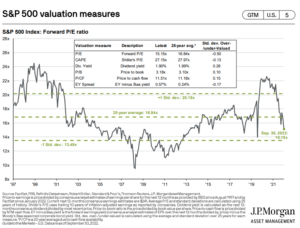

With the S&P 500 down approximately 20% year-to-date and trading below its 25-year average earnings at around 15.5x earnings, we are maintaining a cautious approach as new opportunities are emerging and are ready to take advantage of these opportunities as they present themselves.

Sevasti Balafas, CFA, CPWA®

CEO & Founder

GoalVest Advisory

Source: YCharts, BlackRock, JP Morgan Asset Management, Invesco

According to the Administration for Community Living and the Administration on Aging, 70% of individuals turning age 65 will need some form of long-term care during their lifetime1. While long-term care may seem far away, the decision about how to fund long-term care is much closer. The average cost of care for a semi-private room in a nursing home facility in Kansas was $6,296/month in 2021 according to Genworth’s annual Cost of Care Survey2. This can have a significant impact on your financial plan, so it is crucial to determine how to fund this expense. Four strategies to fund long-term care are (1) traditional long-term care insurance, (2) hybrid life insurance, (3) a long-term care annuity, or (4) self-insure by paying out-of-pocket.

Traditional long-term care insurance is exactly that – insurance that is solely focused on mitigating long-term care risk. These policies give you a set daily/monthly benefit amount that can be used for qualified long-term care expenses for a fixed number of years. If your long-term care stay extends beyond the set benefit period, you may find yourself paying for long-term care out of pocket which can be extremely costly. While there is a downside risk to this strategy, if purchased at the right time, traditional long-term care insurance can provide you with a choice benefit amount.

A second alternative is a hybrid life insurance policy. This option is similar to traditional long-term care insurance in that it provides a set benefit amount that can be used for qualified long-term care expenses. However, the death benefit is reduced by the benefits that are paid out. At the same time, though, any death benefit that was not used for long-term care expenses, will still be paid to your beneficiaries at your passing. A hybrid life insurance policy may be the best fit if you are wanting to mitigate the risk of long-term care expenses while also providing for your family members or achieving your legacy goals.

If you are looking for a more stable income stream during retirement and want to mitigate long-term care expenses, an annuity with a long-term care rider may be the best strategy for you. The annuity provides you a monthly “payment” for the remainder of your lifetime. Additionally, depending on the term of the policy, your beneficiary may continue to receive these payments after your passing. If you need long-term care, the long-term care rider on the annuity is activated and increases your monthly “payment.”

Lastly, you can self-insure by paying for long-term care expenses out of pocket. This eliminates the need to pay premiums for insurance, which can potentially be more costly than the benefits received. Self-insuring, however, has its disadvantages such as depleting your assets much quicker than planned. If an individual needs long-term care and their spouse does not, self-insuring poses the risk of leaving the remaining spouse with limited or no assets. Despite the risks, self-insuring may be the best strategy if you have significant assets set aside for healthcare expenses.

Long-term care planning is an important and difficult decision to make. Each person’s situation is unique, and thus the strategy for helping pay for potential long-term care costs should be tailored to them. Before jumping into any long-term care planning, remember to contact your advisor for guidance. It is important to fully understand your options before making such a weighty decision. If you would like more information on, or assistance with, long-term care planning, our advisors are here to help.

Investment advice offered through V Wealth Advisory, LLC, dba Gentry Private Wealth, a registered investment advisor. SEC registration does not constitute an endorsement of Gentry Private Wealth by the SEC nor does it indicate that Gentry Private Wealth has attained a particular level of skill or ability. Information presented is for educational purposes only intended for a broad audience. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments or strategies. Investments involve risks and are not guaranteed.

The firm believes that the content provided by third parties through the links is reasonably reliable and does not contain untrue statements or material fact, or misleading information. This content may be dated.

You are now leaving the Gentry Private Wealth Website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Gentry Private Wealth or any advisor(s) whose name(s) appears on this Website. Gentry Private Wealth is independently owned and operated. Schwab neither endorses nor recommends Gentry Private Wealth. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Gentry Private Wealth under which Schwab provides Gentry Private Wealth with services related to your account. Schwab does not review the Gentry Private Wealth Website, and makes no representation regarding the content of the Website. The information contained in the Gentry Private Wealth Website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.