The Advisor, June 2023

June 6, 2023

Wasn’t it just yesterday that we were wearing our winter coats in the morning and covering our plants to protect them from frost overnight? Just like the snap of our fingers, summer is here! As the seasons change, so do the factors that affect the market. This edition of The Advisor explores the key trends shaping the investment landscape around the globe in GoalVest’s market insight. We also get back to the basics of wealth management by exploring the art of being tax-efficient.

Be sure to check back in July for our Mid-Year market and economic outlook. As always, if you have any questions or would like to discuss anything further, please reach out to our office at (316) 613-7570.

Jeff Wetta, RPS and Dustin Jackson, CFP® RICP®

Managing Partners

The country looks set to avoid default as an agreement on the debt ceiling has passed both the House and Senate. The agreement, dubbed the “Fiscal Responsibility Act,” caps Federal baseline spending for two years in exchange for a raise to the debt ceiling into 2025. Markets have responded positively to the news, with equities up about 3% over the last five days.

Equities and bonds are off to a solid start as we move closer to the end of the second quarter. So far, the rally in the S&P 500 this year has been highly concentrated and driven by a select number of technology companies with exposure to artificial intelligence. Many companies in the S&P 500 are actually down year-to-date, which is evidenced by the performance divergence between the S&P 500 index and the S&P 500 equally-weighted index year-to-date. This is the widest spread we have seen since 1989. We have exposure to these well-performing technology companies through our allocation to VOO & VUG. We also have exposure to some of these companies directly in our core equity portfolio, including Microsoft, Google, and Amazon.

In our Quality High Dividend strategy, we have seen some losses so far this year. Dividend stocks are down 8.8% year-to-date as measured by the iShares Select Dividend ETF. While we have slightly reduced our exposure to our Quality High Dividend strategy, we believe there are still opportunities in quality high dividend stocks. It appears that a number of these companies are trading at compelling valuations and have the potential to deliver solid returns over the next one to five years. We remain confident in their strength, their ability to generate good earnings through the economic cycle, and their ability to pay dividends. Additionally, we are monetizing volatility through structured yield and digital growth notes to incorporate higher returns that we consider attractive in this economic environment. We are also close to finalizing our private equity allocations for eligible investors as we seek risk-adjusted returns through a higher allocation to alternative investments.

Leading economic indicators, such as the yield curve, money supply, and manufacturing new orders data, continue to point towards an economic slowdown. This can be positive for equities, though, if it allows the Fed to pause interest rate increases or potentially cut interest rates down the line. In our view, inflation remains high at about 4.9% (inflation ex-food and energy is even higher), and it will be challenging for the Fed to cut interest rates until inflation moves closer to the 2% target. We think the Fed is likely to pause interest rate increases at their June or July meeting. Since 1980, the S&P 500 has generated a positive return (average of +15%) in the 12 months following a Fed pause in every scenario but one. With this in mind, we continue to focus on driving risk-adjusted returns through our long-term investments in good quality, American businesses, structured notes with compelling return prospects, and a higher allocation to alternative investments.

Sevasti Balafas, CFA, CPWA®

CEO & Founder

GoalVest Advisory

Sources: Bloomberg, Invesco, Goldman Sachs, JP Morgan Asset Management, Ycharts, Blackstone, Deutsche Bank, Wall Street Journal

By: Maria Martin, CFP®

Have you ever thought that, because you contribute to your company’s retirement plan or an IRA, you are doing all you can to be as tax-efficient as possible with your wealth? Unfortunately, it’s not that simple. Tax-efficient investing and planning is a technique that must be carefully thought out and implemented. It’s critical to know what tax diversification is and what types of tax planning strategies you can leverage to improve your overall wealth and financial plan.

Tax Diversification:

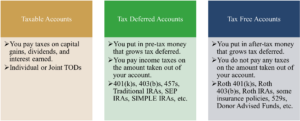

There are two main paths to tax diversification: Types of Accounts and Types of Assets. The below table explains the differences in tax treatment between various types of accounts.1

Consolidating all your wealth into one type of account does not always provide the long-lasting benefit that splitting your wealth between different types of accounts can provide. For high earners not eligible for Roth IRAs, account diversification can become even more challenging. We might take advantage of Roth 401(k)s, indexed universal life insurance policies, and different types of assets to help diversify. The below chart outlines different types of assets and their tax characteristics.

Tax Planning Strategies:

To leverage your overall financial strength, consider implementing specific tax planning strategies that can help reduce your tax liability such as:

Charitable Gifting

Most individuals gift cash to their local church or charity. However, if you have highly appreciated investments in a taxable account, you could gift these shares to the charity instead of giving cash. Gifting the appreciated securities not only reduces your potential tax liability2 but also frees up cash that you can invest or use for other goals.

Investment Management

Tax loss harvesting occurs when you sell assets at a loss to help offset your capital gains. This strategy can be especially helpful when you have large taxable gains during the year and want to reduce the overall tax impact. By realizing losses, you reduce your total taxable gain and therefore your total tax liability.

Each investor’s portfolio is unique to their goals and situation. If you have an annual tax budget, be sure to tell your investment manager so they can select tax-efficient holdings for your portfolio. If you’re in a high tax bracket, you may want to limit your taxable investment income and thus consider investing in tax-free holdings. Or you may plan to hold your securities for at least one year so they are taxed at long-term capital gains rates instead of income tax rates.

Whether you’re in the top tax bracket or just starting out, efficient tax planning can provide long-lasting benefits for your overall financial plan. However, tax law can get complicated, so please be sure to coordinate with your tax professional and financial advisor before making any decisions.

Source: Charles Schwab, IRS.gov

You are now leaving the Gentry Private Wealth Website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Gentry Private Wealth or any advisor(s) whose name(s) appears on this Website. Gentry Private Wealth is independently owned and operated. Schwab neither endorses nor recommends Gentry Private Wealth. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Gentry Private Wealth under which Schwab provides Gentry Private Wealth with services related to your account. Schwab does not review the Gentry Private Wealth Website, and makes no representation regarding the content of the Website. The information contained in the Gentry Private Wealth Website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.