The Advisor, February 2023

February 7, 2023

We’ve heard from Punxsutawney Phil, so we know we’re in for six more weeks of winter. If only predicting the next six weeks in the market were as easy as waking up a groundhog… Although, taking advice from a rodent is probably not a reliable wealth management approach.

This is why we trust investment and economic research to build our investment strategies. In this month’s issue, we review market trends and explore our Economic Outlook for 2023. We’ll also focus on the latest tax and retirement plan updates for 2023.

Markets rallied at the start of 2023. The S&P 500 was up 6.3% as of January 31st, and the US Aggregate Bond index was up 3.3%. Additionally, inflation numbers released in January for the month of December reported a decline to 6.5%. This is still well above Fed’s 2% target, however.

On a positive note, the economy is proving resilient in the face of last years’ interest rate increases. Preliminary Q4 2022 GDP came in ahead of expectations at +2.9%; this has helped drive strong company earnings so far this year. And while most leading indicators point towards an economic slowdown, households still possess more than half of the savings they accumulated during the pandemic ($1.4 trillion). This savings is being depleted by approximately $80 billion per month and could prove to be a cushion in the event of a recession, thus increasing the chance for a “soft landing.”

Inflation is gradually falling, though there is still work to be done. Corporate profits remain solid despite individual weaknesses. The trajectory of interest rate moves later this year will depend on the Fed’s ability to bring services inflation down. At their February meeting, the Fed increased interest rates by 25 basis points (0.25%) – in line with our initial expectations. The S&P 500 is trading around its long-term average of 17x earnings, which demonstrates a moderation in valuations over the last 12 months.

We plan to maintain our balanced portfolio positioning with investments in high quality companies that have solid profit margins, dry powder (in short term treasuries) to invest in emerging opportunities, and structured notes to drive return in an uncertain environment. Our tactical positioning is data-dependent, and as our hedged notes come due, we are poised to redeploy capital into new opportunities.

Sevasti Balafas, CFA, CPWA®

CEO & Founder

GoalVest Advisory

Source: YCharts, BlackRock, JP Morgan Asset Management, Invesco

At the end of 2022, Congress passed the SECURE Act 2.0 prompting changes to retirement and education planning strategies. Below are a few highlights to keep in mind.

Retirement Savings & Roth Accounts:

Starting in 2024, the IRA catch-up contribution will be adjusted annually for inflation.

Starting in 2025, 401(k) and SIMPLE IRA catch-up contributions for individuals between age 60-63 also increases. The current catch-up contribution for individuals over age 50 remains in place, adjusted for inflation.

Roth SIMPLE IRAs and ROTH SEP IRAs are now permitted, allowing employees and employers to save for retirement with after-tax dollars.

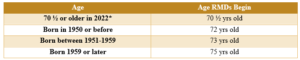

Required Minimum Distribution Changes(RMD):

*If you have already started taking RMDs in 2022, you will continue to take RMDs.

Inherited Spousal IRAs

Starting in 2024, a spouse beneficiary of an Inherited Spousal IRA can elect to be treated as the deceased spouse when it comes to RMD rules. If this election is made, the spouse will follow the Uniform Lifetime Table to calculate their RMD.

Roth 401(k) RMDs

Beginning in 2024, RMDs from Roth accounts in employer-sponsored retirement plans (i.e., 401(k)) are not required.

RMD Penalties

Previously, if you did not satisfy your RMD, you received a 50% excise (penalty) tax on the amount not taken. This was decreased to 25% starting in 2023.

Qualified Charitable Distributions (QCD):

Starting in 2024, the maximum QCD allowed will be increased for inflation. The current maximum QCD is $100,000.

The age you can begin taking QCDs will continue to be age 70 ½.

529 Education Savings Accounts:

Beginning in 2024, if you have a 529 Education Savings Account that has been open for 15 + years for the same beneficiary, you are eligible to transfer up to $35,000 to a Roth IRA for the same beneficiary.

Please note, if the 529 has been open for 15 years, but in year 10, you changed the beneficiary, the 15-year requirement restarts at the time of the beneficiary change.

Any contributions made in the last 5 years, will not be eligible to transfer.

Qualified Retirement Plans:

Penalty-free withdrawal rules have been adjusted to include exceptions for victims of domestic abuse and terminal illness. Additionally, the rules related to qualified disaster relief withdrawals have been adjusted.

Before taking any withdrawals from your qualified retirement plan, please contact your HR department for specific requirements.

If allowed by the plan, plan participants can elect to have their employer contributions deposited as Roth contributions (after-tax dollars). Previously all employer contributions were pre-tax contributions.

Each individual’s financial situation is unique, so please coordinate with your tax professional and financial advisor before making any changes.

Sources: Secure Act 2.0 Update Webinar provided by RightCapital, Secure 2.0 Important Updates provided by EGPS

As always, if you have any questions about any of this information, please do not hesitate to reach out to our office.

You are now leaving the Gentry Private Wealth Website and will be entering the Charles Schwab & Co., Inc. (“Schwab”) Website. Schwab is a registered broker-dealer, and is not affiliated with Gentry Private Wealth or any advisor(s) whose name(s) appears on this Website. Gentry Private Wealth is independently owned and operated. Schwab neither endorses nor recommends Gentry Private Wealth. Regardless of any referral or recommendation, Schwab does not endorse or recommend the investment strategy of any advisor. Schwab has agreements with Gentry Private Wealth under which Schwab provides Gentry Private Wealth with services related to your account. Schwab does not review the Gentry Private Wealth Website, and makes no representation regarding the content of the Website. The information contained in the Gentry Private Wealth Website should not be considered to be either a recommendation by Schwab or a solicitation of any offer to purchase or sell any securities.